Recover Lost, Forgotten, Unclaimed Shares and Dividends of Bajaj Holdings & Investment Limited

If you have recently discovered that you are the legal heir or owner of lost/forgotten/unclaimed shares of Bajaj Holdings and Investment, and you want to recover them, then this is the resource for you.

To recover lost, forgotten, and unclaimed shares and dividends of Bajaj Holdings & Investment Limited, reach out to Share Samadhan. Share Samadhan is Delhi’s foremost lost share recovery company, and they will help you recover your lost, unclaimed shares.

About Bajaj Holdings & Investment Limited

Bajaj Holdings & Investment Limited is one of India’s leading investment and financial holding companies, and a key part of the renowned Bajaj Group.

Established in 1945 and headquartered in Pune, the company primarily focuses on strategic investments, wealth creation, and long-term value generation through its holdings in flagship Bajaj Group companies, including Bajaj Auto and Bajaj Finserv.

Following the 2007 demerger of the erstwhile Bajaj Auto Limited, Bajaj Holdings & Investment Limited emerged as the Group’s principal investment arm, managing a diversified portfolio across equity, debt, and other financial assets.

With a strong legacy of financial discipline, prudent investment strategies, and sustainable growth, the company continues to play a vital role in strengthening the Bajaj Group’s long-term vision while also contributing to social development through impactful CSR initiatives in healthcare, education, employability, and community welfare.

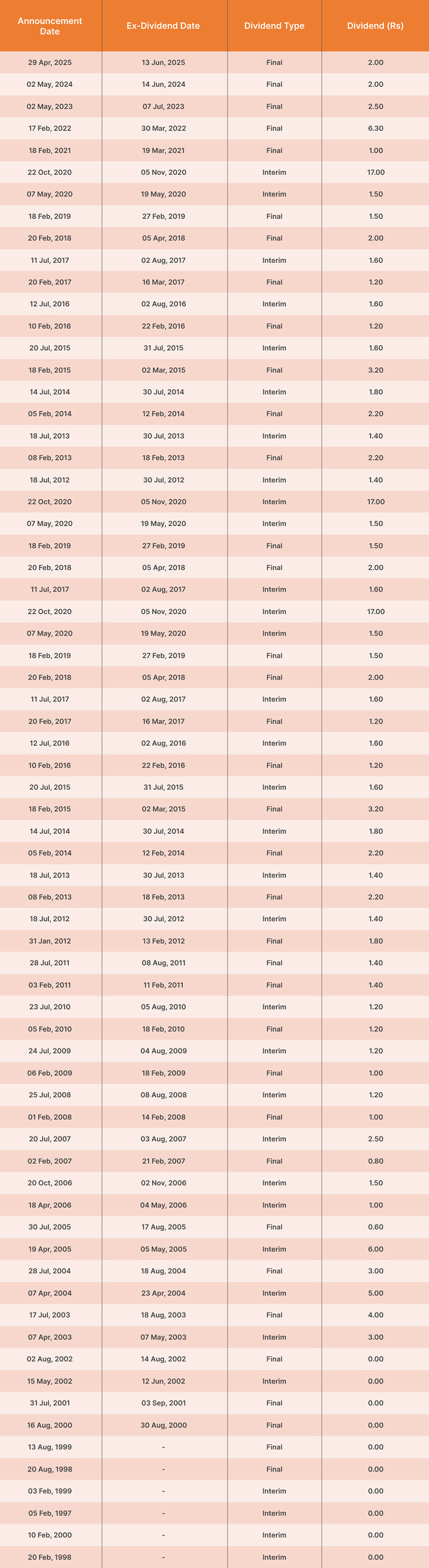

Historical Data on the Shares Issued by Bajaj Holdings and Investment Limited

Bajaj Holdings & Investment Limited does not have a conventional IPO history available in the way modern companies do today because it originated from the restructuring and demerger of the erstwhile Bajaj Auto Limited in 2007. The company became a separately listed entity after the Bajaj Group reorganization rather than through a fresh public IPO.

Here are the key listing and share details available:

-

Incorporation Date: 29 November 1945

-

Public Listing / Demerger: 2007

-

Stock Exchanges: BSE & NSE

-

BSE Code: 500490

-

NSE Symbol: BAJAJHLDNG

-

ISIN: INE118A01012

-

Face Value: ₹10 per share

-

Market Lot: 1 share

The company emerged after the demerger of Bajaj Auto Limited into:

-

Bajaj Auto Limited

-

Bajaj Finserv Limited

-

Bajaj Holdings & Investment Limited

Because of this structure, there was no traditional IPO issue price, price band, or subscription process recorded for Bajaj Holdings & Investment Limited. Existing shareholders of Bajaj Auto received shares in the newly formed entities after the demerger.

How to Recover Unclaimed Dividends and Shares of Bajaj Holdings & Investment Limited from IEPF

To reclaim any lost, forgotten, and unclaimed dividends or shares of Bajaj Holdings & Investment Limited from IEPF, follow these 5 steps.

Step 1: First, you need to check for unclaimed shares and dividends on the IEPF website.

Go to the official IEPF website and use the “Search Unclaimed/Unpaid Amounts” option. Enter details such as the company name, investor name, PAN, Folio Number, or DP ID to check whether any unclaimed amounts are pending under your name.

Step 2: Download and fill out Form IEPF-5

Visit the MCA portal and fill out Form IEPF-5 by providing details such as your PAN or Aadhaar number, demat account information, dividend details, and share or folio particulars. After submission, download the acknowledgment receipt along with a copy of the completed form for your records.

Step 3: Submit the documents to the Nodal Officer

Print the completed IEPF-5 form and submit it along with the necessary documents—such as self-attested copies of PAN and Aadhaar, indemnity bond, proof of entitlement, and original share certificates (if applicable)—to the Nodal Officer or Registrar of Bajaj Holdings & Investment Limited for verification and processing.

Step 4: Verification by the company

The Nodal officer or registrar will verify the claim and review it. After verification, the company forwards a report to the IEPF Authority, typically within 30–60 days.

Step 5: Refund and transfer by the IEPF Authority

Once the IEPF Authority approves the claim, the unclaimed dividend amount is credited to your bank account, and the shares (if any) are transferred back to your demat account.

How Can Share Samadhan Help You with Their Share Recovery Services?

Share Samadhan is a well-known share recovery firm in Delhi that has been offering share recovery services for over 14 years. They help both residential Indians and NRIs in their attempts to recover lost or forgotten shares and dividends of various companies from the IEPF Authority.

IEPF claims can often be complex and time-consuming, particularly for NRIs who may need to travel multiple times to arrange documents and complete the formalities. Many individuals who start the IEPF recovery process become discouraged after a few months, underestimating the effort and patience required to see the claim through successfully.

Share Samadhan simplifies the share recovery process by assigning a dedicated manager to guide you through every step of the claim procedure.

If you have lost, forgotten, or unclaimed dividends and shares of Bajaj Holdings & Investment Limited, you can contact us at 8800332200 or email us at samadhan@sharesamadhan.com.

We help resolve a wide range of issues that may arise during the share recovery process:

-

Demat of shares

-

Unclaimed dividends

-

Proof of legal heir

-

Claims process

-

Important document creation and verification

Conclusion

Share Samadhan simplifies the process of reclaiming unclaimed Bajaj Holdings & Investment Limited shares and dividends from the IEPF, ensuring a smooth and hassle-free recovery experience through a structured approach. You can get in touch with Share Samadhan for professional assistance in recovering your shares and unclaimed dividends.

Frequently Asked Questions

-

How long does the share recovery process take?

It takes around 8 months to 1.5 years at the latest to complete the share recovery process with the assistance of Share Samadhan.

2. What is the address of the RTA and Nodal Officer of Bajaj Holdings & Investment Limited?

The Registrar & Share Transfer Agent (RTA) and IEPF Nodal Officer details for Bajaj Holdings & Investment Limited are:

Registered Office

Mumbai-Pune Road, Akurdi, Pune – 411035, Maharashtra, India.

IEPF Nodal Officer

Mr. Saurabh Erande

Nodal Officer – IEPF

Email: saurabh.erande@bajajfinserv.in

Phone: (020) 7157 6066

Registrar & Share Transfer Agent (RTA)

KFin Technologies Limited

Selenium Tower B, Plot No. 31-32,

Gachibowli Financial District, Nanakramguda,

Serilingampally, Hyderabad – 500032, Telangana, India.

Phone: (040) 6716 2222 / 1800 309 4001

Email: einward.ris@kfintech.com