How to Recover Lost, Forgotten, and Unclaimed Shares of Jindal Steel & Power Limited

A significant amount of investor wealth remains unclaimed in the Investor Education and Protection Fund (IEPF). According to the latest figures, the IEPF Authority holds more than 117 crore unclaimed shares and over ₹8,200 crore in unpaid dividends. These assets belong to investors and their legal heirs who have yet to initiate an IEPF claim. If your dividends have remained unclaimed for seven consecutive years, your shares may have been transferred to the IEPF. Understanding the IEPF claim process can help you recover unclaimed investments and reclaim what is rightfully yours.

You may have recently discovered the old physical shares of Jindal Steel & Power Limited, or you may be the legal heir to shares of Jindal Steel & Power Limited. If you have not claimed dividends in the past 7 years, not even once, your shares have been transferred to IEPF, and it’s time to make an IEPF claim. To recover your shares stuck with IEPF, follow the procedure given in this blog.

About Jindal Steel & Power Limited

Jindal Steel & Power Limited (JSPL) is one of India's leading steel and energy companies. Established in 1979, the company has built a strong presence across steel manufacturing, mining, and power generation. It is known for producing high-quality steel products that support infrastructure, construction, railways, automotive, and industrial development. With integrated manufacturing facilities and advanced technology, JSPL continues to contribute to India's economic growth and industrial progress.

The company operates state-of-the-art steel plants and power projects in India while maintaining a growing international footprint. Its diverse product portfolio includes rails, structural steel, plates, coils, wire rods, and specialty steel solutions that cater to domestic and global markets. JSPL focuses on operational excellence, innovation, and sustainable manufacturing practices. Continuous investments in technology, research, and process improvements enable the company to deliver reliable, high-performance products across industries.

Jindal Steel & Power Limited is committed to responsible business practices and long-term value creation. The company actively invests in environmental conservation, community development, education, healthcare, and skill enhancement through its corporate social responsibility initiatives. By combining world-class manufacturing capabilities with a customer-centric approach, JSPL continues to strengthen its position as a trusted partner in the global steel and power sector while supporting India's vision for sustainable industrial development.

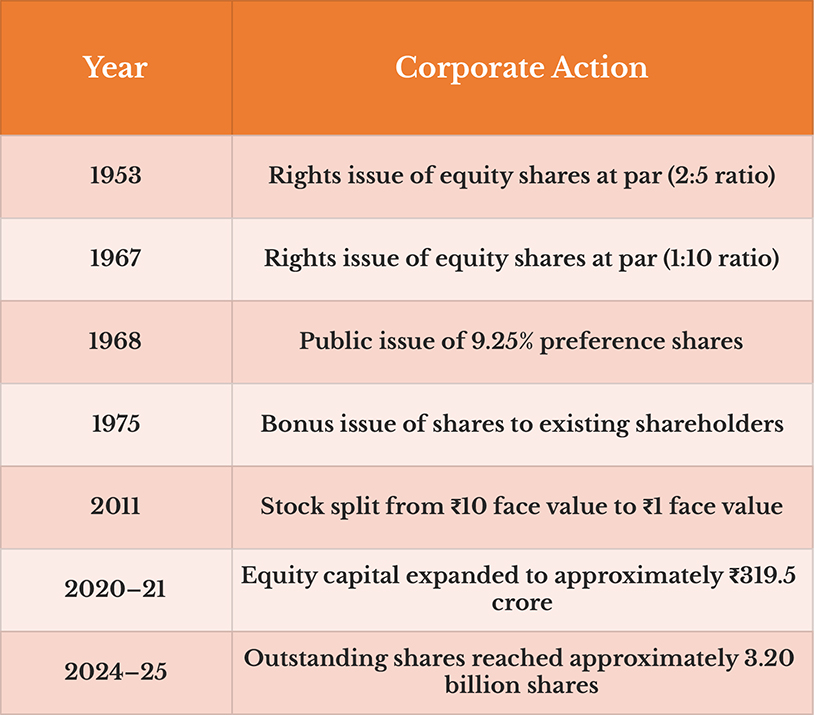

Historical Data on the Shares Issued by Jindal Steel & Power Limited

The share capital history of Jindal Steel & Power Limited (JSPL) reflects the company's steady growth, expansion, and strategic corporate actions over the years. Since its incorporation, the company has raised capital through public issues, preferential allotments, rights issues, and bonus share issuances to support capacity expansion, acquisitions, and business development. These events have played an important role in shaping the company's capital structure and enhancing shareholder value.

Like many listed companies, JSPL has also undertaken corporate actions such as stock splits, bonus issues, and dividend distributions at different stages of its journey. Investors holding physical share certificates issued decades ago may find that the original certificates have undergone changes due to these corporate actions. It is important to verify the current status of old share certificates before initiating a transfer, dematerialisation, transmission, or sale.

In cases where dividends remained unclaimed for seven consecutive years, the corresponding shares may have been transferred to the Investor Education and Protection Fund (IEPF) as per applicable regulations. Shareholders or their legal heirs can recover these shares by following the prescribed IEPF claim process. Reviewing the historical share issuance records and corporate actions can help investors establish ownership and simplify the process of reclaiming unclaimed shares or dividends.

How to Recover Lost, Forgotten, and Unclaimed Shares of Jindal Steel & Power Limited

The first thing you need to do is check whether your shares have been transferred to IEPF or not. Under the provisions of the Companies Act, 2013, companies are required to transfer shares to the Investor Education and Protection Fund (IEPF) if the dividends on those shares remain unclaimed for seven consecutive years. Along with the shares, all unpaid dividends related to those holdings are also transferred to the IEPF Authority. After this transfer, investors cannot recover their shares or dividends through the company. Instead, they must submit an IEPF claim and complete the prescribed recovery procedure to reclaim their investments.

-

How to check shares transferred to IEPF

To check whether your shares have been transferred to the Investor Education and Protection Fund (IEPF), visit the Investor Relations section of Jindal Steel & Power Limited's website. The company periodically publishes a list of shareholders whose unpaid dividends and corresponding shares have been transferred to the IEPF Authority. You can search these records using your name, folio number, DP ID, or Client ID. If your details appear in the list, it indicates that your shares and any associated unpaid dividends have been transferred to the IEPF.

You can also verify the status of your unclaimed shares and dividends through the IEPF Authority's online portal. If you need additional assistance, you may contact Jindal Steel & Power Limited's Registrar and Transfer Agent (RTA) or the company's designated IEPF Nodal Officer. They can help confirm the transfer status and guide you through the next steps for recovering your shares and dividends from the IEPF.

-

Find the Required Documents for Filing an IEPF Claim

Before starting the application, ensure that the following documents are available with you:

-

Entitlement Letter issued by Berger Paints India Ltd. or its Registrar and Transfer Agent

-

Aadhaar Card

-

PAN Card

-

Passport, OCI Card, or PIO Card (where applicable)

-

Corporate Identification Number (CIN) of Berger Paints India Ltd.

-

Folio Number and Demat Account Details

-

Bank Account Information

-

Indemnity Bond and Affidavit

-

Succession Certificate, Probate, or Will (for claims by legal heirs)

-

Death Certificate of the shareholder (where applicable)

-

No Objection Certificates (NOCs) from legal heirs, if required

Having complete and accurate documentation can significantly improve the chances of a successful claim and reduce processing delays.

-

Submit Form IEPF-5 Through the MCA Portal

Once you have created your account on the MCA portal with your email ID and collected all the necessary supporting documents, complete and submit Form IEPF-5 online to initiate your claim. While filling out the form, ensure that the information provided is accurate and matches the records maintained by Jindal Steel & Power Limited and its Registrar and Transfer Agent (RTA).

Carefully verify details such as your name, folio number, DP ID/Client ID, bank account information, and shareholding particulars before submission. Any mismatch between the information entered in Form IEPF-5 and the company's records may lead to processing delays, additional document requests, or rejection of the claim. Accurate documentation helps ensure a smoother and faster IEPF claim process.

-

Send Physical Documents to Jindal Steel & Power Limited

After submitting Form IEPF-5 through the MCA portal, print the completed form and send it, along with all the required supporting documents, to the designated IEPF Nodal Officer of Jindal Steel & Power Limited or its Registrar and Transfer Agent (RTA). Clearly mention "Claim for Refund from IEPF Authority" on the envelope to facilitate timely processing.

The physical document set typically includes:

-

Duly signed copy of Form IEPF-5

-

SRN acknowledgement generated after successful online submission

-

Original Indemnity Bond executed on the prescribed stamp paper

-

Original Advance Stamped Receipt signed by the claimant and witnessed by two individuals

-

Proof of share ownership, such as original physical share certificates or a Demat account statement

-

Self-attested copy of Aadhaar Card

-

Self-attested copy of PAN Card

-

Cancelled cheque or bank passbook copy showing the claimant's name and account details

-

Demat Client Master List (CML), where applicable

-

Passport, OCI Card, or PIO Card for NRI or foreign claimants

-

Any additional declarations, succession documents, or legal certificates, if applicable

Before dispatching the documents, verify that all copies are complete, signed, and self-attested wherever required. It is also advisable to keep photocopies of the entire document set along with the courier receipt or postal acknowledgement for future reference and claim tracking.

-

Verification by Jindal Steel & Power Limited and Processing by the IEPF Authority

Once the physical documents are received, Jindal Steel & Power Limited (JSPL) reviews the claim and verifies the information submitted against its shareholder records. After completing the verification process, the company prepares a verification report and forwards it to the Investor Education and Protection Fund (IEPF) Authority within the prescribed timeline.

The IEPF Authority then examines the claim independently to ensure that all documents, declarations, and supporting evidence comply with the applicable rules. If the claim satisfies all requirements, the Authority approves the application and issues a refund sanction order for the transfer of shares and payment of any eligible unpaid dividends.

Upon approval, the recovered shares are credited electronically to the claimant's Demat account, while the approved dividend amount is transferred directly to the registered bank account. This completes the IEPF claim process and restores the ownership of the shares and dividends to the rightful shareholder or legal heir. Since recovering shares from the IEPF involves multiple documents and strict procedural requirements, many investors choose to seek professional guidance to ensure accurate filing and avoid unnecessary delays in recovering their Jindal Steel & Power Limited shares and dividends.

Why Should You Give Shares Recovery Services a Try?

Shares recovery is a time-consuming process. If your documents have issues like misspelled names, signature mismatch, and other issues, it can be very difficult to get your IEPF claim passed. Also, most people are trying to claim the shares of their deceased parents. Since they are the legal heirs, they have to get a legal heir certificate and other documentation to prove that they are the legal heirs to the shares. This can become a time-consuming process. Sometimes, certain documents may even be missing. To get these documents reissued can take time. Hence, people seek shares recovery services to check if it is feasible to get their shares back, to help them get their documents in order, and finally make a consolidated claim. Since we can make only one claim per company per year, people strive to ensure that their claim is accurate.

Conclusion

Approach Share Samadhan, a premier share recovery firm in Delhi, to assist you with the lost share recovery from IEPF. We help with IEPF claims, transfer and transmission of shares, and duplicate issue of shares.

You can set up a meeting with our team, and if we approve of your case, we will assign you a Dedicated Account Manager who will help you throughout the share recovery process.

NRIs need not worry, as we help with the issue of duplicate share certificates and IEPF shares search. NRIs need not travel back and forth since the whole process will be done online.

Reach out to Share Samadhan today.

Frequently Asked Questions

1. How can I find my lost investments?

You can find lost investments by checking old share certificates, Demat account statements, dividend warrants, bank records, and tax documents. If the shares were listed and dividends remained unclaimed for seven consecutive years, they may have been transferred to the Investor Education and Protection Fund (IEPF). You can also search the company's Investor Relations page or the IEPF portal.

2. How do I recover lost funds from old investments?

Lost funds recovery usually involves identifying the investment, verifying ownership, and submitting the required claim. If your shares or dividends have been transferred to the IEPF, you must file Form IEPF-5 along with supporting documents to recover them.

3. What is an unclaimed investment?

An unclaimed investment refers to shares, dividends, bonds, deposits, or other financial assets that have remained inactive or unclaimed by the investor for a prolonged period. In certain cases, these assets are transferred to the IEPF Authority as required by law.

4. How can I find old shares registered in my name?

You can locate old shares by reviewing physical share certificates, Demat statements, dividend records, bank statements, or family financial documents. You may also contact the company's Registrar and Transfer Agent (RTA) or check the IEPF records if you believe the shares have been transferred.

5. What happens to unclaimed dividends transferred to the IEPF?

Unclaimed dividends are transferred to the IEPF after remaining unpaid for seven consecutive years. They can be recovered by filing Form IEPF-5 and completing the prescribed verification process.

6. How do I perform an IEPF unclaimed shares search?

You can search for unclaimed shares by visiting the Investor Relations section of the concerned company's website or the IEPF Authority portal. Search using your name, folio number, DP ID, or Client ID to verify whether your shares have been transferred.

7. What is the procedure for issuing a duplicate share certificate?

If your physical share certificate has been lost, stolen, or damaged, you must apply to the company or its Registrar and Transfer Agent for a duplicate share certificate. The process generally requires an indemnity bond, affidavit, identity proof, address proof, and other prescribed documents.

8. What is share transmission?

Share transmission is the process of transferring shares to the legal heir or nominee after the death of a shareholder. Unlike a share transfer, transmission takes place by operation of law and requires documents such as the death certificate, succession certificate, probate, or legal heir certificate.

9. How do I claim IEPF shares?

To claim IEPF shares, you must file Form IEPF-5 through the MCA portal, submit the required documents to the company, and complete the verification process. Once approved by the IEPF Authority, the shares are transferred to your Demat account.

10. How can I recover shares from the IEPF?

Recovering shares from the IEPF involves verifying your eligibility, filing Form IEPF-5, submitting physical documents to the company, and waiting for verification by both the company and the IEPF Authority before the shares are restored.